Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. In partnership with Bloomberg Law, Dan has developed a series of 25 articles looking at these trends, on a topic-by-topic basis, providing practical insight into where these trends are heading, and the relevant implications for M&A deal professionals.

Market Trends: What You Need to Know

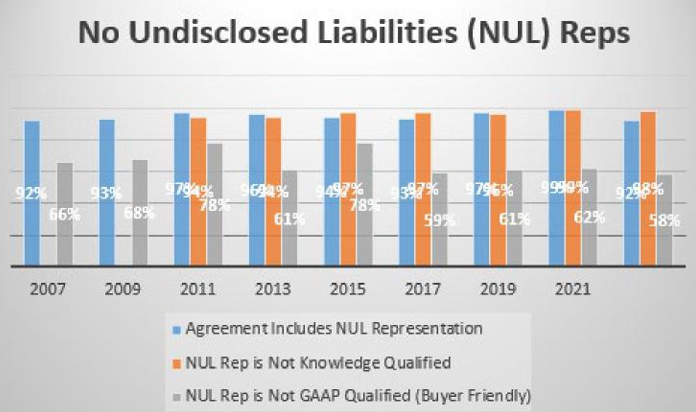

As reflected in the American Bar Association's Private Target Mergers and Acquisitions Deal Point Studies:

- Mergers and acquisitions (M&A) purchase agreements almost universally include a “no undisclosed liabilities” (NUL) representation. Specifically, across the nine ABA studies, a NUL representation was included in 92% to 99% of reported transactions.

- The six most recent ABA studies examined the use of knowledge qualifiers within NUL representations and show that these qualifiers are very rare, appearing in only 1% to 6% of reported transactions with NUL representations.

- Finally, NUL representations are usually (in approximately 60-80% of reported transactions) not qualified by references to Generally Accepted Accounting Principles (GAAP), though over the past 10+ years, the seller-friendly GAAP qualification is becoming more commonly seen, though still a minority position.

Introduction

In M&A transactions, unknown target liabilities are typically addressed in different ways throughout the M&A purchase agreement. A no undisclosed liabilities representation is one of the principal representations in an M&A purchase agreement pursuant to which the seller and buyer allocate the risk of unknown target liabilities amongst themselves.

What Is a No Undisclosed Liabilities Representation?

NUL representations may take various forms, but generally involve the seller making statements to the buyer certifying as to the absence of target liabilities that are not otherwise identified or disclosed (whether addressing specific liabilities or referencing all liabilities).

The buyer typically wants the seller to make an unqualified NUL representation to the extent possible. Specifically, it wants to ensure the representation includes minimal exceptions and covers the maximum universe of potential liabilities. A buyer-friendly version of an NUL representation may read:

The Target has no liabilities of any type whatsoever except for: (i) liabilities reflected or reserved against in the Latest Balance Sheet; and (ii) those liabilities set forth on Schedule X.

The seller, of course, often seeks to limit the scope of liabilities subject to the NUL representation. For example, it typically attempts to incorporate as many exceptions and qualifiers as possible thereby limiting its overall exposure. The seller's efforts to limit its potential liability for breach of an NUL representation usually take one or more of the following forms:

Limiting the Subject Liabilities to GAAP Balance Sheet Liabilities

Because an NUL representation often references a target's balance sheet, a seller may argue that the NUL representation should apply only to the subset of liabilities required under applicable accounting standards to be reported on such a a balance sheet. In an NUL representation including this limitation, the seller need only disclose liabilities of the type required to be reflected as liabilities on a balance sheet prepared in accordance with GAAP. This is an important distinction – – because not all liabilities need be reported under GAAP. For example, under GAAP, the disclosure of contingent liabilities depends upon a number of different factors, including relative probability. In addition, an operating business generally has many ordinary course business liabilities that are not typically liabilities included in a GAAP balance sheet (e.g., normal, but significant contract obligations). And, because truly “unknown” liabilities cannot be disclosed on a balance sheet, they would be excluded as well. In short, GAAP liabilities can be a relatively narrow subset of a target's known and unknown liabilities.

An example of an NUL representation including this limitation may read along the following lines:

The Target has no liability of a nature required to be disclosed in a balance sheet prepared in accordance with GAAP except for: (i) liabilities reflected or reserved against in the Latest Balance Sheet; and (ii) those liabilities set forth on Schedule X.

Adding an “Ordinary Course” Carve-Out

The seller often seeks a carve-out for ordinary course liabilities incurred since the balance sheet date. An example of an NUL representation including this carve-out may read:

The Target has no liability of the nature required to be disclosed in a balance sheet prepared in accordance with GAAP except for: (i) liabilities reflected or reserved against in the Latest Balance Sheet; (ii) liabilities incurred in the Ordinary Course of Business since the date of the Latest Balance Sheet; and (iii) those liabilities set forth on Schedule X.

Including Knowledge or Materiality Qualifiers

The seller may also limit an NUL representation to those undisclosed liabilities of which the seller had knowledge and/or to undisclosed liabilities above a materiality or other threshold.

Excluding Liabilities Which are the Subject of Other Representations

A seller may also object to an NUL representation as being overly broad, and, with respect to any specific topic, potentially in conflict with other representations contained in the purchase agreement specifically covering that topic. For example, if the purchase agreement has a detailed representation regarding environmental matters that requires disclosure of liabilities arising under environmental laws in excess of $10,000, should the NUL representation separately require disclosure of environmental liabilities below $10,000? An example of this type of limitation to the NUL representation – – excluding matters which are the subject of disclosure requirements elsewhere in the purchase agreement – – may read:

The Target has no liability … except for: … (iv) liabilities which are disclosed on any other Schedules or which are not required to be disclosed under any representation or warranty in Article X because of a materiality, dollar or knowledge threshold or qualifier.

The Buyer's Position

The buyer often insists on a broad NUL representation because, from its point of view, the seller should bear at least some risk of undisclosed or unknown liabilities. To make its point, the buyer often argues that the seller is in a better position than the buyer to assess the risk of unknown liabilities because of the seller's familiarity with the past and current operations of the target company, and therefore should be expected to stand behind its assessment.

In practice, however, where NUL representations are present, they are usually included within the category of seller representations that are subject to an indemnity basket and cap—i.e., a minimum level of buyer loss before seller responsibility kicks in, as well as a stated maximum amount of seller liability. In this context, the buyer is already assuming some of the risk of unknown liabilities even with a normal, “buyer-friendly” NUL representation (specifically, those unknown liabilities of amount within the basket and above the cap). Often those unknown liabilities are also addressed in more topic-oriented representations throughout the agreement – – with respect to, for example, compliance with laws, employment matters, tax compliance and the like. Thus, in deal negotiations, NUL representations are often described – – particularly if broad in scope – – by sellers as redundant or duplicative.

The Seller's Position

The seller may argue one or more of the following to attempt to negate the buyer's arguments:

- If the purchase agreement covers in great detail all aspects of the target's business, why is a broader “catch-all” representation needed or appropriate?

- If the parties have agreed that certain types of contracts and other liabilities are not required to be disclosed under specific seller representations, why should those thresholds be ignored for an NUL representation?

- Other provisions in the purchase agreement afford the buyer adequate protection against certain liabilities. In support of this argument, sellers most often cite (i) the standard seller representations with respect to the target's financial statements and (ii) that no material adverse effect has occurred since a specified date.

Trends in Usage of No Undisclosed Liabilities Representations

Every other year since 2005 the ABA has released its Private Target Mergers and Acquisitions Deal Point Studies (the “ABA studies”). The ABA studies examine purchase agreements of publicly available transactions involving private companies. These transactions range in size but are generally considered as within the “middle market” for M&A transactions; the transaction values of the 123 deals within the 2021 study ranged from $30 to $750 million.

According to the ABA studies, M&A purchase agreements consistently include an NUL representation. Specifically, across the nine ABA studies, an NUL representation was included in 92% to 99% of reported transactions. Additionally, the six most recent ABA studies examined the use of knowledge qualifiers within NUL representations and found that these qualifiers are rare, appearing in only 1% to 6% of reported transactions. Finally, non-GAAP qualified NUL representations (i.e., “all liabilities” coverage, the buyer favored approach) are much more common than the seller-favored GAAP-qualified versions, appearing in 58% to 78% of reported transactions.

The chart below shows these trends.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

Conclusion

The NUL representation remains near-universal in private company M&A transactions. Seller attempts to use knowledge qualifiers to limit exposure have been met with very little success. Additionally, the seller-friendly GAAP-only NUL representation continues to be a minority approach, though much more common than knowledge qualifiers. As discussed above, these qualifiers impact allocation of undisclosed liabilities as between buyer and seller. Counsel on both sides of an M&A transaction should consider these issues carefully when negotiating an NUL representation.

Click here for a pdf of the article.

Reproduced with permission from Bloomberg Law. Copyright ©️2022 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bloomberglaw.com.

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-22-16-48-04-221-662694c48171a252db3820bd.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-22-15-12-36-997-66267e64d100dba38ac045e7.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-22-13-15-13-552-662662e18171a252db378c86.png)

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-10-02-23-24-827-6615f81c7f643c6b40a522fc.png)