Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. In partnership with Bloomberg Law, Dan has developed a series of 25 articles looking at these trends, on a topic-by-topic basis, providing practical insight into where these trends are heading, and the relevant implications for M&A deal professionals.

Market Trends: What You Need to Know

RWI is an increasingly important feature of private company merger and acquisition transactions. Every other year since 2005 the ABA has released its Private Target Mergers and Acquisitions Deal Points Studies (the “ABA studies”). The most recent three of these studies (2017, 2019 and 2021) have looked at representation and warranty insurance (“RWI”) in private company M&A transactions.

As shown in these three most recent ABA studies:

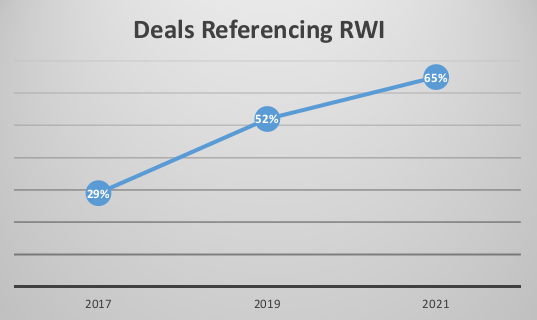

- RWI References. The percentage of transactions expressly referencing RWI increased from 29% in the 2017 study, to 52% in the 2019 study, to 65% in the 2021 study.

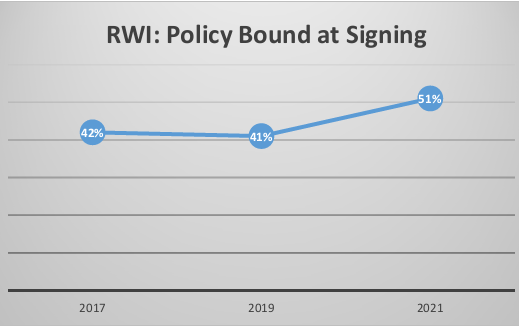

- Bound at Signing. Of the deals with RWI reported in the three studies, 42%, 41% and 51%, respectively, expressly required the RWI policy to be bound at the signing of the purchase agreement.

- Who Acquires the Policy? The buyer acquired the RWI policy in 93%, 95% and 95%, respectively, of the RWI deals reported in the three studies.

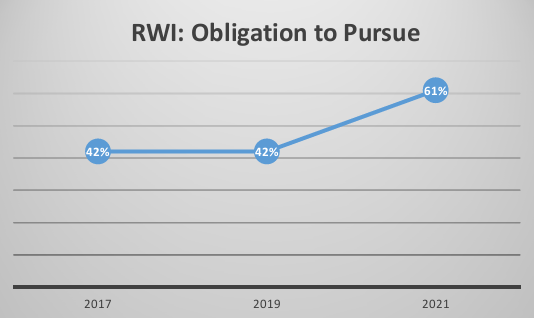

- Obligation to Pursue RWI. An indemnitee's obligation to first pursue RWI coverage was included in 42%, 42% and 61% of RWI transactions, in the three studies.

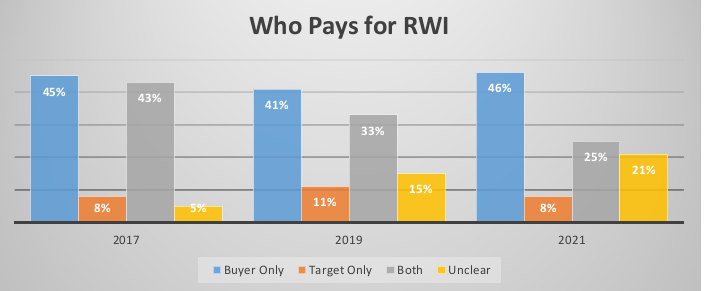

- RWI Payment. In most cases, the buyer bore full, or shared with the seller, responsibility for RWI premium payments. The seller bore full responsibility for payment in 10% or so of reported transactions in the three studies.

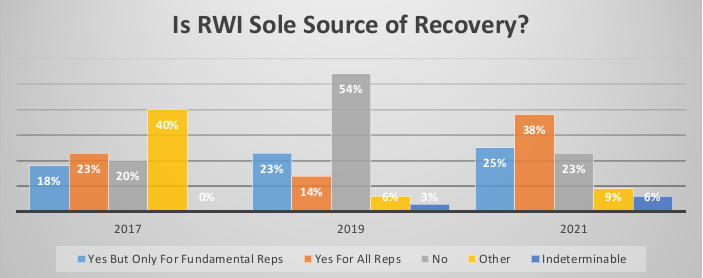

- RWI as Sole Source of Recovery. Express negative statements to the effect that RWI is not the sole source of recovery were included in 20%, 54% and 23%, respectively, of reported transactions within the three studies between 2017 and 2021.

Introduction

In M&A transactions, the definitive purchase agreement (whether asset purchase agreement, stock purchase agreement, or merger agreement) typically contains representations and warranties made by the seller with respect to the target company. Representations and warranties not only provide information to the buyer, but also operate to allocate risk as between the buyer and seller with respect to the matters covered by the representations and warranties.

Historically, sellers were responsible for damages suffered by buyers and caused by breaches of the seller's representations and warranties, through indemnification provisions. Pursuant to indemnification provisions, any given party would agree to defend, hold harmless, and indemnify the other party or parties from specified claims or damages. Those defense and indemnification obligations are often limited by time, dollar levels, and/or types of claims and damages.

In the past 12 plus years, buyers and sellers have been able to outsource the exposure to buyers from breaches of seller representations and warranties to third party insurers issuing RWI policies. This article looks at the ways that RWI is addressed in private company M&A agreements, as reflected in the relevant ABA studies.

The Growth of RWI

One of the biggest changes in private company M&A during the past decade has been the enormous growth of RWI. With RWI, buyers and sellers are able to allocate some of the post-closing M&A indemnity risk to third party insurers. RWI has gone from being a differentiator that aggressive buyers offered to a much more common feature of private M&A deals. As indemnity risk has been shifted through RWI from sellers to third party insurers, avenues for a buyer's indemnity recourse against sellers have narrowed, including through the lowering of indemnity caps and even the elimination of post-closing seller indemnity for representations and warranties (subject to narrow exceptions, such as in the event of fraud).

The most recent three ABA studies have looked at certain RWI-related provisions in reported private company M&A agreements. It is worth noting, however, that relying solely on explicit references to RWI in M&A transaction documents as evidence of RWI's usage is potentially imperfect. In the author's experience, sellers may insist that they have minimal involvement with or “connection” to the RWI insurer or the RWI process, and that the buyer should deal with indemnity risk wholly on its own, whether through RWI, self-insurance, and/or negotiations with the seller in the M&A documents. In that context, there may be no need or desire for any explicit reference to RWI in the executed agreements. This approach is driven at least partly by the concern that if faced with claims, insurers may seek third party beneficiary, subrogation, privity or other means of recourse against the seller (notwithstanding language in the documents to the contrary), and the view that reducing any documentary connections with, or even references to, RWI could assist in a seller defense against such insurer claims. In addition, where the seller, and not the buyer, is acquiring the RWI policy (admittedly a relatively rare circumstance), one would expect there to be no need to reference the policy in the M&A documents (though those situations would likely not see an impact on seller indemnity caps or baskets). As a result, it is possible if not likely that some meaningful number of M&A deals with RWI have no references in the deal documents to the insurance policy itself or to RWI generally.

Trends in RWI

The ABA studies examine purchase agreements of publicly available transactions involving private companies. These transactions range in size but are generally considered as within the “middle market” for M&A transactions; the transaction values of the 123 deals within the 2021 study ranged from $30 to $750 million.

The ABA Study in 2017 was the first to review the use of RWI in private M&A transactions. Accordingly, ABA study data is limited to three of the nine ABA studies (2017, 2019 and 2021). Given the growth of RWI, it is fully expected that future ABA studies will continue to look at RWI.

Basic RWI Data

RWI References

The percentage of transactions expressly referencing RWI increased from 29% in the 2017 study, to 52% in the 2019 study, to 65% in the 2021 study.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

Bound at Signing

Of the deals with RWI reported in the three studies, 42%, 41% and 51%, respectively, expressly required the RWI policy to be bound at the signing of the purchase agreement.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

Who Acquires the Policy?

The buyer acquired the RWI policy in 93%, 95% and 95%, respectively, of the RWI deals reported in the three studies.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

Obligation to Pursue RWI

An indemnitee's obligation to first pursue RWI coverage was included in 42%, 42% and 61% of RWI transactions, in the three studies.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

RWI Payment

In most cases, the buyer bore full, or shared with the seller, responsibility for RWI premium payments. The seller bore full responsibility for payment in 10% or so of reported transactions.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

RWI as Sole Source of Recovery

Express negative statements to the effect that RWI is not the sole source of recovery were included in 20%, 54% and 23%, respectively, of reported transactions within the three studies between 2017 and 2021.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

Conclusion

RWI is an increasingly important feature of private company M&A transactions. Since only the three most recent ABA studies looked at RWI, data is still too light to identify many trends beyond the fact that RWI is now seen in more than half of reported private company transactions. Even in the absence of long term data, it seems clear that RWI will continue to be an option for buyers and sellers looking to allocate representation and warranty indemnity risk beyond the primary transaction parties.

Click here for a pdf of the article.

Reproduced with permission from Bloomberg Law. Copyright ©️2022 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bloomberglaw.com

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-10-02-23-24-827-6615f81c7f643c6b40a522fc.png)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-03-26-18-33-10-871-660314e6a95774bc3ec2d0f5.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-01-19-48-49-062-660b0fa164547688f7bc778e.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-03-28-14-07-08-054-6605798c002b00c29f61ce55.jpg)