Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. In partnership with Bloomberg Law, Dan has developed a series of 25 articles looking at these trends, on a topic-by-topic basis, providing practical insight into where these trends are heading, and the relevant implications for M&A deal professionals.

Market Trends: What You Need to Know

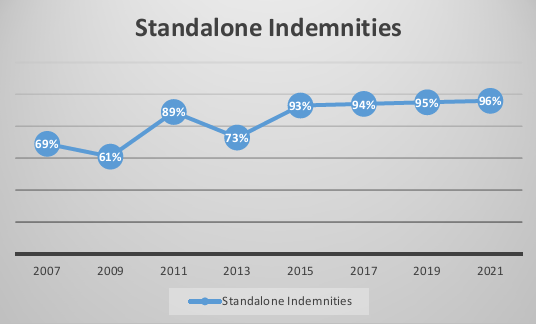

According to the American Bar Association's nine Private Target Mergers and Acquisitions Deal Points Studies, the use of stand-alone indemnities in reported private company M&A transactions has increased from 69% in its 2007 study to 96% in 2021. This article examines the prevalence and usage of stand-alone indemnities in private company M&A transactions with reference to the ABA studies.

Introduction

In private company M&A transactions, the indemnification provisions of a definitive purchase agreement—whether asset purchase agreement, stock purchase agreement, or merger agreement—stand out in importance for both buyers and sellers. Standard indemnification provisions in M&A purchase agreements typically provide that the “indemnitor” (the party providing indemnification) will indemnify, defend, and hold harmless the “indemnitees” (the parties receiving indemnification) for losses incurred by the indemnitees as a result of the indemnitor's breach of representations, warranties, covenants, or other obligations under the transaction documents.

These “general indemnities” are often subject to various limitations, including limits on the amounts available for recovery and how long the indemnities survive closing, and usually address breaches of the purchase agreement or other ancillary documents—e.g., breaches of representations, warranties, or covenants.

In addition to the general indemnities, the parties to M&A agreements often negotiate separate “stand-alone” indemnities that cover specific topics outside the general indemnities, usually without reference to an underlying breach of the representations, warranties, or covenants.

Stand-Alone Indemnities

Generally speaking, stand-alone indemnities cover two types of matters:

- Matters for which the buyer does not wish to assume any post-closing responsibility, regardless of whether those matters constitute a breach otherwise covered in the purchase agreement, or arose as a particular concern during the buyer's diligence.

- Matters arising during the buyer's diligence that pose unusual or unexpected risk.

The first category of matters may include tax, ERISA, and environmental liabilities, or other “excluded” liabilities, and target indebtedness and transaction expenses—e.g., investment banking, accounting, and legal fees. Using taxes as an example, a buyer may, not unreasonably, argue that it should never be responsible for paying the seller's taxes, regardless of whether a breach of the tax representation has occurred. Further, it may argue that the seller's liability to pay its taxes should not be subject to a basket, cap, or time period shorter than that otherwise applicable.

The second category covers matters that the buyer may discover during the M&A due diligence process that warrant singling out and covering with a stand-alone indemnity. The stand-alone indemnity reallocates the risk of losses that may have an adverse impact on the target's business post-closing.

For example, the buyer might learn during its due diligence that the target's best-selling consumer product may contain traces of lead potentially harmful to children, something both material and presumably unexpected. The buyer will be concerned about the potential financial loss resulting from product liability lawsuits and possible damage to the product's brand name and reputation—exposure that the buyer may not have considered in assessing and pricing the transaction. As such, the buyer may require that seller provide a stand-alone indemnity to cover any associated losses.

A typical indemnity section of an M&A purchase agreement may read:

Indemnification by the Seller. The Seller agrees to and will defend and indemnify the Buyer Parties and save and hold each of them harmless against, and pay on behalf of or reimburse such Buyer Parties for, any Losses which any such Buyer Party may suffer, sustain or become subject to, as a result of, in connection with, relating or incidental to or arising from:

(i) any breach by the Seller of any representation or warranty made by the Seller in this Agreement or any Additional Closing Document;

(ii) any breach of any covenant or agreement by the Seller under this Agreement or any Additional Closing Document;

(iii) any of the matters set forth on Schedule [___];

(iv) any Taxes due or payable by the Company or its Affiliates with respect to any Pre-Closing Tax Periods; or

(v) any Company Indebtedness or Company Expenses to the extent not repaid or paid, respectively, pursuant to Section [___] and not included in the purchase price adjustment pursuant to Section [___].

In this provision, clauses (i) and (ii), which are tied to breaches of representations, warranties, and covenants, are general indemnities and clauses (iii), (iv), and (v) are stand-alone indemnities.

In addition to general indemnities typically being connected with a breach, there are often other differences between general and stand-alone indemnities. For instance, general indemnities are usually subject to both “baskets” (whereby the indemnitor is not liable for breaches until a specific threshold of indemnitee losses are reached) and caps (limiting the indemnitor's overall liability for breaches). Further, the underlying representations and warranties to which the general indemnities apply often expire after a prescribed time period, usually prior to the otherwise applicable statute of limitations.

Of course, there are often exceptions to these general constructs. For example, representations and warranties that the parties determine are “fundamental”—e.g., those regarding title, authority, taxes, and ERISA—may be subject to the general indemnities but have no basket or cap, or a different basket or cap, and different expiration period. In contrast, stand-alone indemnities are not often subject to baskets, caps, or specific time periods, though the parties are free to, and sometimes do, negotiate specific baskets, caps, and expiration dates for these indemnities.

Despite the differences, there may be overlap and some redundancy between general and stand-alone indemnities. For example, the sample provision above includes a common stand-alone indemnity relating to pre-closing taxes. However, the typical M&A purchase agreement also includes a tax representation, which is often not subject to a basket or cap, that would typically be covered by the general indemnity.

Buyer & Seller Perspectives

Most M&A purchase agreements include representations, warranties, and covenants from both the seller to the buyer, and the buyer to the seller. However, as a practical matter, the scope of representations, warranties, and covenants and related indemnities from the seller are usually much broader in scope and substance than those from the buyer. This is not surprising because the seller's representations and warranties cover a wide range of financial and operating matters relating to the target. In contrast, the buyer's representations and warranties typically focus on its ability to consummate the transaction and perform its obligations.

Accordingly, the seller is usually more inclined to limit the scope of indemnities overall, regardless of whether they are general or stand-alone indemnities. The buyer, on the other hand, has a corresponding desire to expand the scope of indemnities to the broadest extent possible.

Trends in Stand-alone Indemnity Provisions

Every other year since 2005 the ABA has released its Private Target Mergers and Acquisitions Deal Points Studies. The ABA studies examine purchase agreements of publicly available transactions involving private companies. These transactions range in size but are generally considered as within the “middle market” for M&A transactions; the transaction values of the 123 deals within the 2021 study ranged from $30 to $750 million.

Since 2007, the percentage of transactions including these indemnities increased from 69% to 96% in 2021. The chart below shows this trend.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

According to the 2021 study, 32% of the agreements included stand-alone indemnities on dissenter's claims (compared to 32% in 2019), 39% on unpaid seller transaction expenses (compared to 57% in 2019), 5% on ERISA issues (compared to 3% in 2019), 8% on environmental issues (compared to 6% in 2019), 72% on taxes (compared to 78% in 2019), and 91% on “other” issues (compared to 85% in 2019).

Prior to 2015, the ABA studies did not separately track stand-alone indemnities on dissenters’ claims or unpaid seller transaction expenses, instead the studies included these indemnities in the other issues category. ERISA and environmental-related stand-alone indemnities continues to be relatively rare, and, in contrast, tax-related stand-alone indemnities are much more common.

Additionally, the “other issues” category of stand-alone indemnities also saw significant fluctuation between 2007 and 2021, with the percentage of agreements including stand-alone indemnities not related to ERISA, environmental, or tax ranging from 43% (2009) to 91% (2021).

Overall, a significant percentage of transactions examined in the seven most recent ABA studies include one or more standalone indemnities.

Assuming that the ABA studies reasonably reflect general practice in M&A transactions, it appears that, after a slight pullback in 2012, the usage of stand-alone indemnities overall reached a peak in 2020-2021, as reported in the 2021 ABA study. Stand-alone indemnities for ERISA and environmental issues seem to be consistent, and relatively rare, while stand-alone indemnities for tax and other issues are more commonplace.

Additionally, the inclusion in the more recent ABA studies of stand-alone indemnities for dissenters’ claims and for unpaid seller transaction expenses as separate data points indicates that these two areas have become increasingly important areas of negotiation.

Conclusion

Stand-alone indemnities are not typically subject to the same limitations as general indemnities, nor do they depend upon an underlying breach by the indemnifying party. As such they may more readily shift risk back to the indemnitor when compared to general indemnities, even if both cover the same risks. Accordingly, practitioners should carefully consider these provisions in the overall context of the transaction and the agreed-upon risk allocation as between buyer and seller.

Click here for a pdf of the article.

Reproduced with permission from Bloomberg Law. Copyright ©️2022 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bloomberglaw.com

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-22-16-48-04-221-662694c48171a252db3820bd.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-22-15-12-36-997-66267e64d100dba38ac045e7.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-22-13-15-13-552-662662e18171a252db378c86.png)

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-10-02-23-24-827-6615f81c7f643c6b40a522fc.png)