Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. In partnership with Bloomberg Law, Dan has developed a series of 25 articles looking at these trends, on a topic-by-topic basis, providing practical insight into where these trends are heading, and the relevant implications for M&A deal professionals.

Market Trends: What You Need to Know

Over the past 15+ years covered by the ABA studies, materiality scrapes have morphed from being a somewhat uncommon provision, seen in about 14% of transactions in 2005, to something near-ubiquitous in M&A purchase agreements, now included in 92% of transactions. M&A deal points tend to evolve gradually, and slowly; in relative terms, increased inclusion of materiality scrapes in M&A purchase agreements reflects one of the most dramatic trends covered by the ABA studies.

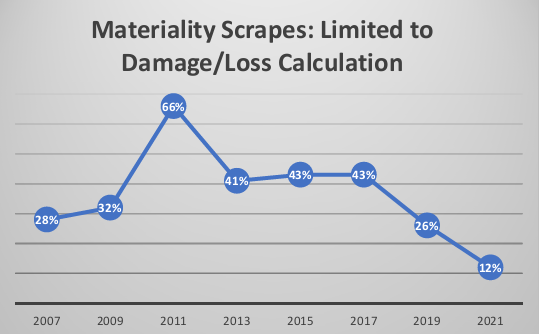

Occasionally, buyers and sellers adopt a “compromise” position as to materiality scrapes whereby materiality is not disregarded (i.e., is not scraped) when determining whether a breach has occurred; but is disregarded (i.e., is scraped) in determining the losses or damages resulting from that breach (i.e., damages are not limited to whether or not they were material). Such a compromise provision might read along the following lines: “For the purpose solely of determining indemnified Losses, but not for the purpose of determining whether a breach of a representation or warranty shall have occurred, any materiality or Material Adverse Effect qualifiers or references in the Seller's representations and warranties shall be disregarded.” This approach seems to have fallen into relative disfavor, and is currently seen in only about 12% of reported transactions.

Introduction

A “materiality scrape” is a buyer-friendly provision often contained in an M&A purchase agreement (such as a stock purchase agreement, merger agreement, or asset purchase agreement) that effectively eliminates or disregards (i.e., “scrapes”), for specified purposes, materiality qualifiers that are otherwise present in a representation and warranty. See examples of materiality scrapes below.

In terms of apportioning responsibility for a target company's liabilities as between buyer and seller in an M&A transaction, a “materiality scrape” can be one of the most important provisions within the transaction documents. And yet this provision―and its significance to the overall risk profile of an M&A transaction―is often not fully understood or appreciated.

This article is intended to summarize the effect and implications of a materiality scrape, as well as to identify related market trends for private company M&A transactions. These trends are reflected in the American Bar Association's Private Target Mergers and Acquisitions Deal Point Studies, which cover U.S. M&A transactions involving privately held targets.

What Is a ‘Materiality Scrape’?

As sellers and buyers negotiate M&A purchase agreements, sellers seek to limit the potential for those representations and warranties to be proven wrong and to result in a buyer claim. One way in which sellers pursue this goal is to narrow the scope of representations and warranties, including by adding materiality, knowledge, or other qualifiers to the relevant language. For example, a representation by the seller that “the target company is not party to any material litigation” is narrower in scope than the same statement without the word “material.” The typical materiality scrape provision eliminates materiality qualifiers from one or more sections of the purchase agreement. Using the example above if a purchase agreement contains a materiality scrape, the representation and warranty that states “the target company is not party to any material litigation” would be read, in determining whether a breach of that representation and warranty has occurred for indemnification purposes, as “the target company is not party to any litigation.” In other words, the statement is read as if the word material was never included in the first place—the materiality qualifier otherwise applicable to the representation is “scraped” away.

A materiality scrape provision is sometimes referred to as a “double” or “blanket” materiality scrape if it applies to determining both whether or not a breach has occurred and the amount of indemnified losses resulting from that breach. Although including a double materiality scrape is common in purchase agreements, as noted below, applying a materiality scrape to the determination of losses resulting from a breach, but not as to whether or not the breach occurred (a “single” materiality scrape), is occasionally utilized as a compromise approach to this deal point.

The types of breaches most commonly subject to a materiality scrape are breaches of representations and warranties. Occasionally, though much less typically, covenants (i.e., obligations to do, or refrain from doing, something) or agreements are subject to a materiality scrape.

The qualifiers most commonly subject to a scrape are materiality and material adverse effect (MAE). Occasionally, though rarely, seen is a “knowledge scrape,” which eliminates knowledge qualifiers from representations and warranties (or covenants).

Materiality & MAE Qualifiers

Materiality and MAE qualifiers serve different purposes within a purchase agreement, and the materiality scrape usually eliminates these qualifiers for some but not all of those purposes. Materiality and MAE qualifiers generally serve four different purposes:

- Determining whether closing conditions have been satisfied (e.g., closing conditions may require that the seller's representations and warranties be true and correct “in all material respects” at the closing or that there be no MAE in effect as of the closing).

- Determining the scope of the seller's disclosure (e.g., a representation may affirmatively require disclosure of all “material” contracts).

- Determining whether a breach of a representation has occurred (e.g., whether specific facts are contrary to the seller's representation that it has complied with applicable laws “in all material respects”).

- Determining the losses resulting from such a breach (in other words, where a representation is qualified by materiality, are the resulting losses that are subject to indemnity only those above a “material amount”?).

Implementation

Materiality scrapes are generally either embedded within the indemnification provisions of the purchase agreement or set forth as a standalone provision. The following (with italics added for emphasis) is an example of an embedded materiality scrape provision:

The Seller shall indemnify, defend and hold harmless the Purchaser and its Affiliates and their respective employees, officers, directors, stockholders, partners and representatives from and against any losses, assessments, liabilities, claims, damages, costs and expenses (including reasonable attorneys’ fees and disbursements) incurred by such indemnified party as the result of any misrepresentation in, breach of or failure to comply with, any of the representations, warranties, covenants or agreements of the Seller contained in this Agreement, in each case, with respect to any such representation or warranty, as if such representation or warranty would read if all qualifications as to materiality, including each reference to the defined term “Material Adverse Effect,” were deleted therefrom.

Comparatively, a “standalone” materiality scrape provision (covering only representations and warranties) may read:

For purposes of determining whether there has been a breach and the amount of any losses that are the subject matter of a claim for indemnification, each representation and warranty in this Agreement will be read without regard and without giving effect to the term “material” or “material adverse effect” (fully as if any such word or phrase were deleted from such representation and warranty).

The Buyer's Position

The buyer's arguments for requesting a materiality scrape provision generally take the form of one or more of the following:

Fill the Indemnity Basket. A typical purchase agreement contains a indemnity “basket,” which is intended to provide the seller (as the indemnifying party) protection from general indemnity claims below a certain negotiated amount. Thus, the basket protects the seller against “immaterial” claims. However, materiality or MAE qualifiers throughout the representations and warranties arguably create a “double materiality” threshold for the buyer to “fill the basket” before indemnity is triggered.

Consequently, absent a materiality scrape, the buyer could incur many losses as the result of unrelated breaches of the seller's representations and warranties that are not individually material but are material in the aggregate, and such losses would not count toward the basket. Where agreements also have, in addition to a basket, a “de minimis threshold” (often called a “mini-basket”)—i.e., claims of less than $X are not covered by indemnification nor counted towards the basket―the buyer can argue that the absence of a materiality scrape creates a “triple materiality” threshold.

Eliminate Post-Closing Materiality Disputes. Eliminating materiality and MAE qualifiers can help reduce or eliminate post-closing disputes between the parties as to what is and what is not “material.”

Clarify Breach/Loss Issue. The materiality scrape provision eliminates the potential seller argument that the materiality qualifier applies to the level of recoverable losses, not just to breach, and takes the uncertainty out of this issue (to the extent there is uncertainty).

Streamline Negotiations. By reducing the significance of materiality and MAE qualifiers generally and across the board for purposes of determining allocation of risk of breach (and loss), the negotiation of the purchase agreement becomes more efficient, as the parties need not negotiate every usage of those qualifiers with the same level of attention.

The Seller's Position

Not surprisingly, sellers have a different view of the world when it comes to materiality scrape provisions. Sellers’ arguments against including a materiality scrape usually include the following:

‘Close & Sue.’ If a materiality scrape eliminates materiality and MAE qualifiers from determining existence of a breach but not from determining whether closing conditions have been satisfied, the effect is that a seller can be forced to close “into a breach” and be held accountable immediately after closing for that breach.

‘Nickeling & Diming.’ The buyer should absorb some level of risk of loss in connection with the acquisition of a business, and a materiality scrape allows or even encourages buyers to hunt for any claim, no matter how minor, to pursue against the seller.

Increased Disclosure Burden. If materiality and MAE qualifiers are to be read out of the representations and warranties requiring either affirmative disclosure (e.g., “Schedule 4.3 sets forth all material contracts”) or negative disclosure (e.g., “except as set forth on Schedule 4.4, the seller is in compliance with all applicable laws in all material respects”), the seller will be forced to disclose everything and anything, even if immaterial and of no real interest to the buyer, creating significant inefficiencies.

Awkward Application in Certain Situations. Eliminating materiality and MAE qualifiers from certain representations and warranties creates potentially awkward results. For example:

- If the seller represents that there has been no MAE since a certain date (a common representation), how can MAE be deleted from that statement?

- The normal financial statement representation is usually tied to the GAAP standard that the financial statements “fairly present in all material respects” the financial condition of the target. Do the parties intend to deviate from the established GAAP standard via a materiality scrape provision?

- The typical “full disclosure” representation is based on the language of Rule 10b-5 of the Securities Exchange Act of 1934 that the seller's statements (and/or other information provided in connection with the transaction) do not contain any untrue statement of material fact or omit to state a material fact necessary to make any of the statements, in light of the circumstances in which they were made, not misleading. Similar to the GAAP issue above, are the parties intending to alter the normal 10b-5 standard?

- Some representations and warranties may not be subject to the indemnification basket, most typically those relating to title, taxes, ERISA, and brokers’ fees. In the absence of a basket, should the materiality and MAE qualifiers remain in place in those representations?

Common Compromises

Some possible compromises to deal with the different perspectives of the seller and buyer include the following ways to lessen the impact of a materiality scrape:

- Use a true “deductible” basket (where the basket amount is never recoverable but rather serves as a deductible against buyer claims) instead of a “tipping basket” (where the basket amount is recoverable from dollar one once the aggregate buyer claims exceed the basket amount). Using a deductible basket, which is pro-seller, arguably supports the rationale for a materiality scrape.

- Increase the amount of the deductible basket or tipping basket.

- Rely on specific dollar thresholds within the representations and warranties in lieu of materiality or MAE qualifiers.

- Have the materiality scrape apply to the determination of losses resulting from a breach, but not as to whether or not the breach occurred, i.e., implement a single materiality scrape in lieu of a double materiality scrape. This proposed compromise, as discussed above, arguably has substantive flaws and is increasingly uncommon in reported transactions.

- Except from the materiality scrape any affirmative disclosure requirements, so that the seller need not disclose immaterial matters within its disclosure schedules.

- Specify that the materiality scrape does not apply to certain specific representations and warranties—e.g., the financial statement and full disclosure representations, and/or representations that are not subject to a basket.

Trends in Usage of Materiality Scrape Provisions

A materiality scrape is a pro-buyer provision. Accordingly, when M&A markets are buyer-friendly, one would expect to see greater usage of materiality scrapes (and vice versa).

Every other year since 2005 the American Bar Association has released the ABA studies. The ABA studies examine publicly available purchase agreements of transactions involving private companies. These transactions range in size but are generally considered as within the “middle market” for M&A transactions; the transaction values of the 123 deals within the 2021 study ranged from $30 to $750 million.

The ABA studies show a relatively steady increase in the presence of materiality scrape provisions from 2004 through the last study. Most private company M&A deal points have relatively stable usage and trends in any direction usually are slow and incremental, particularly if relating to a deal point that has meaningful impact on risk allocation as between buyer and seller. The shift in practice norms for materiality scrapes over the 15+ years covered by the ABA studies is, in that context, therefore remarkable.

In the 2005 study, only 14% of the reported deals had materiality scrapes, but by 2019 that mix had completely changed. In the last ABA study, 92% of reported transactions included a materiality scrape. The chart below reflects this significant change in M&A practice.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

As indicated above, an occasional compromise position between buyer and seller is to allow for a single materiality scrape. Using the litigation representation example, above, that “the target company is not party to any material litigation,” this compromise position would mean that: (a) materiality would not be scraped in determining whether a breach had occurred, so that non-material litigation would not trigger a breach; but (b) materiality would be scraped in determining the losses or damages resulting from that breach (i.e., damages would not be limited to whether or not they were material).

The common criticism of this compromise is that it offers very little to the buyer seeking the materiality scrape in the first instance. Most lawyers would assert that a materiality qualifier in a party's representation qualifies the representation only and, absent specific language to the contrary, has no direct bearing on calculating damages once the representation is breached. In other words, scraping materiality from damages calculation simply states the obvious, reflecting what would happen under normal contract principles, and therefore provides little or nothing to the party seeking a materiality scrape.

As shown by the chart below, this compromise position is becoming increasingly less common, likely for those reasons.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

The real focus of the materiality scrape, and where it has substantive impact, is on the determination of a breach of the representation qualified by materiality, not on resulting damages. More recently buyers and sellers appear to have adopted this view and have generally disfavored limiting materiality scrapes to damage calculations.

Conclusion

The materiality scrape is here to stay and, as the ABA studies indicate, has, in one form or another, become almost universally present in private company M&A transactions. Of course, as with any substantive provision in an M&A agreement, inclusion of a materiality scrape depends on how the provision fits with the overall allocation of risk between buyer and seller, the attractiveness of economic or other substantive terms, and the relative negotiating strength of the parties. A materiality scrape packs a lot of punch within a relatively small amount of wording, and practitioners should carefully consider the impact and operation of such a provision within their deal documents.

Click here for a pdf of the article.

Reproduced with permission from Bloomberg Law. Copyright ©️2022 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bloomberglaw.com

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-10-02-23-24-827-6615f81c7f643c6b40a522fc.png)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-03-26-18-33-10-871-660314e6a95774bc3ec2d0f5.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-01-19-48-49-062-660b0fa164547688f7bc778e.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-03-28-14-07-08-054-6605798c002b00c29f61ce55.jpg)