Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. In partnership with Bloomberg Law, Dan has developed a series of 25 articles looking at these trends, on a topic-by-topic basis, providing practical insight into where these trends are heading, and the relevant implications for M&A deal professionals.

Market Trends: What You Need to Know

As reflected in the American Bar Association's Private Target Mergers and Acquisitions Deal Points Studies:

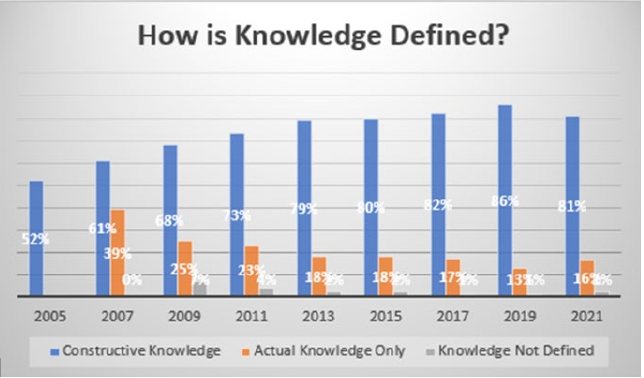

- “Knowledge” is now almost always defined in private company transaction agreements. For example, in the 2021 study only 2% of the reported deals left knowledge undefined.

- The definition of knowledge increasingly includes both constructive and actual knowledge (instead of mere actual knowledge alone). Specifically, including constructive knowledge has steadily increased over the nine ABA studies— from 52% of reviewed deals in the 2005 ABA study to 81% in the most recent 2021 study (down slightly from 86% in the 2019 study).

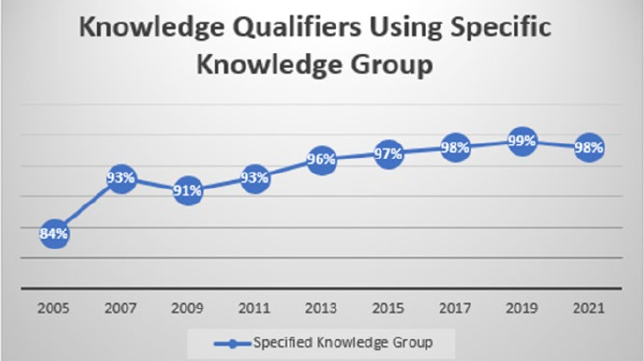

- Over the course of the nine studies, a large and increasing percentage of reviewed deals define a “knowledge group” to include specific individuals. In the 2021 study, nearly all (98%) of the reported deals referred to a knowledge group or specific individuals.

Introduction

In merger and acquisition (M&A) transactions, the definitive purchase agreement typically contains representations and warranties made by the seller with respect to the target company. The scope and detail of these representations and warranties are often heavily negotiated and tailored to reflect both the nature of the target and its business, financial condition and operations, but also the relative negotiating strength of the buyer and seller. Representations and warranties not only provide information to the buyer, but also allocate risk as between buyer and seller with respect to the covered matters.

During negotiations the seller typically attempts to keep its representations and warranties as narrowly drawn as possible while the buyer wants to broaden the seller's representations and warranties. One approach a seller can use to limit the scope of its representations and warranties is to include knowledge qualifiers.

In addition to knowledge, there are other possible qualifiers, including qualifiers relating to materiality, material adverse effect (MAE), and dollar thresholds. The buyer, on the other hand, wants the seller's representations and warranties to be unqualified (i.e., “flat” representations and warranties that do not contain any qualifiers).

Even when the parties agree to use a knowledge qualifier, the scope of knowledge must be determined. Is the knowledge only “actual” knowledge, or does it include “constructive” knowledge? And whose knowledge is relevant for the knowledge-qualified representations and warranties? This article examines the use of knowledge qualifiers in private company M&A transactions.

Knowledge Qualifiers

A knowledge qualifier limits the reach of a contractual provision so that the provision only applies to what the relevant party “knows.” A buyer, as noted above, prefers that the seller's representations and warranties are effective regardless of whether the seller had knowledge of a covered matter. An example of a knowledge-qualified representation is: “To the knowledge of the Seller, there is no breach or anticipated breach by any party to any Contract to which the Company is also party.”

Sometimes representations and warranties may be partially qualified by knowledge. Examples of partially qualified representations include:

- No third party has made any claim asserting that any Intellectual Property Rights owned or held by the Company should be transferred to or placed under the control of a third party, nor has any third party made a request or demand that any such transfer be made by the Company other than in an arm's length transaction and in exchange for full and fair market value; and to the Seller's knowledge, the Intellectual Property Rights owned by or licensed to the Company have not been infringed, misappropriated or conflicted by other Persons.

- No notices have been received by and no claims have been filed against the Company alleging a violation of any applicable laws, ordinances, codes, rules, requirements or regulations, and, to the knowledge of the Seller, the Company has not been subject to any adverse inspection, finding, investigation, penalty assessment, audit or other compliance or enforcement action.

- There are no (and, during the five years preceding the date hereof, there have not been any) actions, suits, proceedings, orders, investigations or claims pending or, to the Seller's knowledge, threatened against or affecting the Company or the Assets (or to the Seller's knowledge, pending or threatened against or affecting any of the officers, directors or employees of the Company with respect to their business activities).

Defining Knowledge

A buyer's agreement to a knowledge qualifier in a particular seller representation and warranty usually is not the end of the discussion. The parties must still negotiate the scope of the seller's knowledge.

In general, there are two principal components to this discussion: first, whether the seller's knowledge is limited to actual knowledge, or whether it also includes constructive knowledge; and second, whether the “seller's knowledge” is limited to the knowledge of specifically identified persons (or categories of persons).

Actual vs. Constructive Knowledge

Actual knowledge requires the relevant party to actually know of a particular item or event that causes a breach. An example of an actual knowledge definition is:

Knowledge means, when referring to the “knowledge” of the Seller, or any similar phrase or qualification based on knowledge, the actual and conscious knowledge (but excluding any constructive knowledge) of ….

Constructive knowledge is, in effect, imputed knowledge, so there are potentially different variations of this concept. For example, constructive knowledge could be defined as the knowledge that any given individual would be expected to learn after some reasonable level of diligence, or what that individual would be expected to know in his or her capacity as an officer, director, or employee, etc. (as applicable) of the target. Examples of constructive knowledge definitions include:

- Knowledge means, when referring to the “knowledge” of the Seller, or any similar phrase or qualification based on knowledge, the actual knowledge of [named individuals], and the knowledge that each such person would have reasonably obtained after making due and appropriate inquiry with respect to the particular matter in question.

- Knowledge means, when referring to the “knowledge” of the Seller, or any similar phrase or qualification based on knowledge, the actual knowledge of [named individuals], and the knowledge that each such person would have reasonably obtained after making due and appropriate inquiry with respect to the particular matter in question, including, without limitation, inquiry of [employee X with respect to general topic Y, etc.].

- Knowledge means, when referring to the “knowledge” of the Seller, or any similar phrase or qualification based on knowledge, the actual knowledge of [named individuals], and the knowledge that each such person would have reasonably obtained in the performance of each such person's duties as [Chief Executive Officer, President, etc.] of the Company.

Identification of Specific Persons

Some definitions limit knowledge to one or more specifically identified persons whose knowledge is taken into account for the knowledge definition. Buyers and sellers often negotiate the individuals who will be included within (or excluded from) the “knowledge group.”

From a buyer's perspective, the knowledge group should include those individuals having control over, and in any event those most likely to have knowledge of relevant facts with respect to, the items covered by the relevant knowledge qualified representations and warranties. In smaller, closely held corporations with a small group of shareholders active in the business, it may be appropriate to have all shareholders in the knowledge group. When the seller is a larger company with multiple operational functions, specific individuals might be included in the knowledge group for selected representations (e.g., including the seller's human resources director as to the employment and HR representations or the risk management director with respect to insurance).

Trends as to Knowledge Qualifiers

Every other year since 2005 the ABA has released its Private Target Mergers and Acquisitions Deal Points Studies. The ABA studies examine purchase agreements of publicly available transactions involving private companies. These transactions range in size but are generally considered as within the “middle market” for M&A transactions; the transaction values of the 123 deals within the 2021 study ranged from $30 to $750 million.

The ABA studies show that knowledge is almost always defined in private company transactions. For example, in the 2021 study only 2% of the reported deals left knowledge undefined. The studies also reveal that the definition of knowledge increasingly includes both constructive and actual knowledge (instead of mere actual knowledge alone). In fact, defining knowledge to include constructive knowledge has steadily increased over the nine ABA studies—from 52% of reviewed deals in the 2005 ABA study to 81% in the most recent 2021 study (down slightly from 86% in the 2019 study).

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

Additionally, over the course of the nine ABA studies, a large and increasing percentage of deals define a “knowledge group” to include specific individuals. In the 2021 study, nearly all (98%) of the reported deals referred to a limited knowledge group or specific individuals whose knowledge was the subject to the qualifier.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

Conclusion

Buyers and sellers will be expected to negotiate: which seller representations and warranties are to be qualified by knowledge; how knowledge is to be defined (i.e., actual knowledge only, or actual and constructive knowledge); and who is in the knowledge group. As a general proposition (and there are always exceptions to reflect the particulars of any given transaction), knowledge qualifiers are usually most appropriate for facts or matters which are outside the seller's control or which cannot reasonably be determined through the seller's diligence—for example, whether or not litigation is being “threatened” but not yet asserted in the form of a demand notice or complaint.

Counsel on both sides of an M&A deal should carefully consider the use of knowledge qualifiers, both as to which representations they qualify, and also as to whether the qualifiers include actual knowledge or both actual and constructive knowledge, and who is included in the knowledge group. Use of knowledge qualifiers can operate to shift risk for post-closing problems as between buyer and seller, and therefore should be tailored specifically to any particular transaction.

Click here for a pdf of the article.

Reproduced with permission from Bloomberg Law. Copyright ©️2022 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bloomberglaw.com.

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-10-02-23-24-827-6615f81c7f643c6b40a522fc.png)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-03-26-18-33-10-871-660314e6a95774bc3ec2d0f5.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-01-19-48-49-062-660b0fa164547688f7bc778e.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-03-28-14-07-08-054-6605798c002b00c29f61ce55.jpg)