Goulston & Storrs M&A attorney Dan Avery is a nationally recognized expert on M&A deal point trends. In partnership with Bloomberg Law, Dan has developed a series of 25 articles looking at these trends, on a topic-by-topic basis, providing practical insight into where these trends are heading, and the relevant implications for M&A deal professionals.

Market Trends: What You Need to Know

As shown in the American Bar Association's Private Target Mergers and Acquisitions Deal Points Studies:

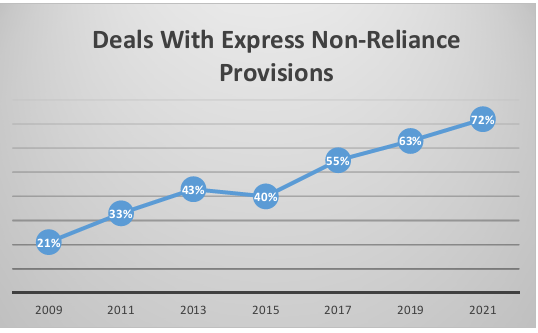

- Express non-reliance provisions are increasingly common in merger and acquisition transactions, and have tripled in prevalence over the seven ABA studies since 2009. These provisions have become the majority approach, appearing in 72% of agreements in 2021.

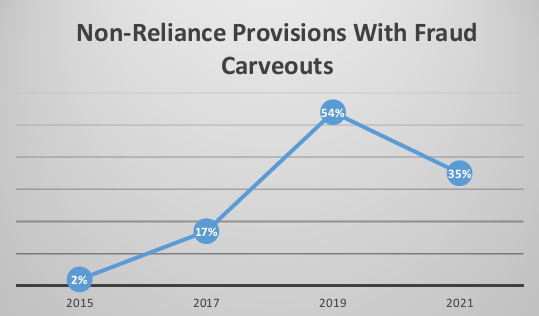

- Fraud carve-outs are increasingly seen in non-reliance provisions, showing a steady and pronounced increase since 2015—from 2% to 17% to 54%.

- The 2019 and 2021 ABA studies also looked at “no other representations” (NOR) provisions and found that 64% and 80% respectively, of the reported transactions included NOR provisions. 60% and 37%, respectively, of those NOR provisions included an express fraud carve-out.

Introduction

In M&A transactions, the definitive purchase agreement—whether asset purchase agreement, stock purchase agreement, or merger agreement—typically contains representations and warranties of the seller, along with related indemnification obligations.

One common concern of a seller is ensuring that its statements outside the four corners of the agreement—e.g., written statements in a marketing document prepared in connection with the transaction or verbal statements of company management made in meetings with the buyer—are not treated as actionable representations.

Sellers accomplish this through a representation that the buyer has not relied on any representations other than those made in the agreement in deciding to effect the transaction—an “express non-reliance” provision. Express non-reliance provisions often are paired with a related provision that states that the representations in the agreement are the only representations given by the seller relating to the transaction—often called a “no other representations” or “NOR” provision). This article examines trends in the use of non-reliance and NOR provisions in private company M&A transactions.

Express Non-Reliance Provisions

The following is an example of a typical non-reliance provision (from the 2015 ABA study):

Buyer acknowledges and agrees that Target has not made and is not making any representations or warranties whatsoever regarding the subject matter of this Agreement, express or implied, except as provided in Section 3, and that it is not relying and has not relied on any representations or warranties whatsoever regarding the subject matter of this Agreement, express or implied, except for the representations and warranties in Section 3.

The example above is a relatively short-form version of the non-reliance language, paired with a NOR provision. Below is a lengthier version of the representation in which the non-reliance language may be found:

Acknowledgement. The Buyer acknowledges that, except for the representations and warranties contained in Article V and Article VI, none of the Sellers nor any Company nor any of their respective directors, managers, officers, employees, Affiliates, controlling persons, agents, advisors or representatives, makes or shall be deemed to have made any representation or warranty, either express or implied, in connection with the transactions contemplated hereby, including as to the accuracy and/or completeness of any information (including, without limitation, any estimates, projections, forecasts or other forward-looking information) provided or otherwise made available to the Buyer or any of its directors, managers, officers, employees, Affiliates, controlling persons, agents, advisors or representatives (including, without limitation, in any virtual data room management presentations, information or offering memorandum, supplemental information or other materials or information with respect to any of the above), that the sole representations or warranties being made by the Sellers or any Company with respect to the transactions contemplated hereby are set forth in said Articles V and VI, and that the Buyer is not relying on any statements, information or data other than the representations or warranties in said Articles V and VI in its determination to effect such transactions. With respect to any estimate, projection or forecast delivered by or on behalf of the Sellers or any Company, the Buyer acknowledges that: (i) there are uncertainties inherent in attempting to make such estimates, projections and forecasts; (ii) the Buyer is aware that actual results may differ materially; and (iii) the Buyer shall have no claim against the Sellers with respect to any such estimate, projection or forecast.

Often, as shown by the ABA studies discussed below, M&A practitioners are carving out fraud as an exception to non-reliance and NOR provisions.

Related Provisions

Express non-reliance provisions are related, at least in part, to three other common components of an M&A purchase agreement:

No Other Representations or NOR Provision. As noted above, a NOR provision states that the representations in the agreement are the only representations given by the seller relating to the transaction.

Sandbagging Provisions. An “anti-sandbagging” provision precludes a buyer from bringing a claim for a breach of representation following the closing if the buyer knew of the breach—or the facts triggering the breach—as of closing. A “pro-sandbagging” clause expressly permits the buyer to pursue such a claim notwithstanding any knowledge.

Exclusivity of Remedies Provision. This clause states that the indemnification provisions in the purchase agreement constitute the sole remedy of the parties to bring claims relating to the transaction, subject to limited exceptions, such as for fraud.

Trends in Express Non-Reliance and NOR Provisions

Every other year since 2005, the ABA has released its Private Target Mergers and Acquisitions Deal Points Studies. The ABA studies examine purchase agreements of publicly available transactions involving private companies. These transactions range in size but are generally considered as within the “middle market” for M&A transactions; the transaction values of the 123 deals within the 2021 study ranged from $30 to $750 million.

The last seven ABA studies illustrate that express non-reliance provisions are increasingly common, tripling in prevalence during that period, and, as of the 2017 study, are the majority approach.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

The last four ABA studies published findings on fraud carve-outs in non-reliance provisions and showed a steady and pronounced increase in these carve-outs from 2015 until 2019, followed by a dip in the most recent ABA study.

GRAPHIC—Source: ABA Private Target Mergers and Acquisitions Deal Points Studies

The 2019 and 2021 ABA studies also looked at “no other representations” (NOR) provisions and found that 64% and 80% respectively, of the reported transactions included NOR provisions. 60% and 37%, respectively, of those NOR provisions included an express fraud carve-out.

Conclusion

Express non-reliance, and NOR, provisions have become increasingly common in M&A purchase agreements. The provisions should not, however, be viewed in a vacuum—rather such provisions can relate to other provisions within the purchase agreement, such as sandbagging and exclusivity of remedies provisions. Counsel for both buyer and seller should consider all of these topics together in the whole when negotiating the M&A purchase agreement.

Click here for a pdf of the article.

Reproduced with permission from Bloomberg Law. Copyright ©️2022 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bloomberglaw.com.

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-22-16-48-04-221-662694c48171a252db3820bd.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/SearchServiceImages/2024-04-22-15-12-36-997-66267e64d100dba38ac045e7.jpg)

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-22-13-15-13-552-662662e18171a252db378c86.png)

/Passle/630ddfd8f636e917dcf6e4ce/MediaLibrary/Images/2024-04-10-02-23-24-827-6615f81c7f643c6b40a522fc.png)